[ad_1]

STARTUPS U/S 54GB . Income Tax Benefit on Investment in

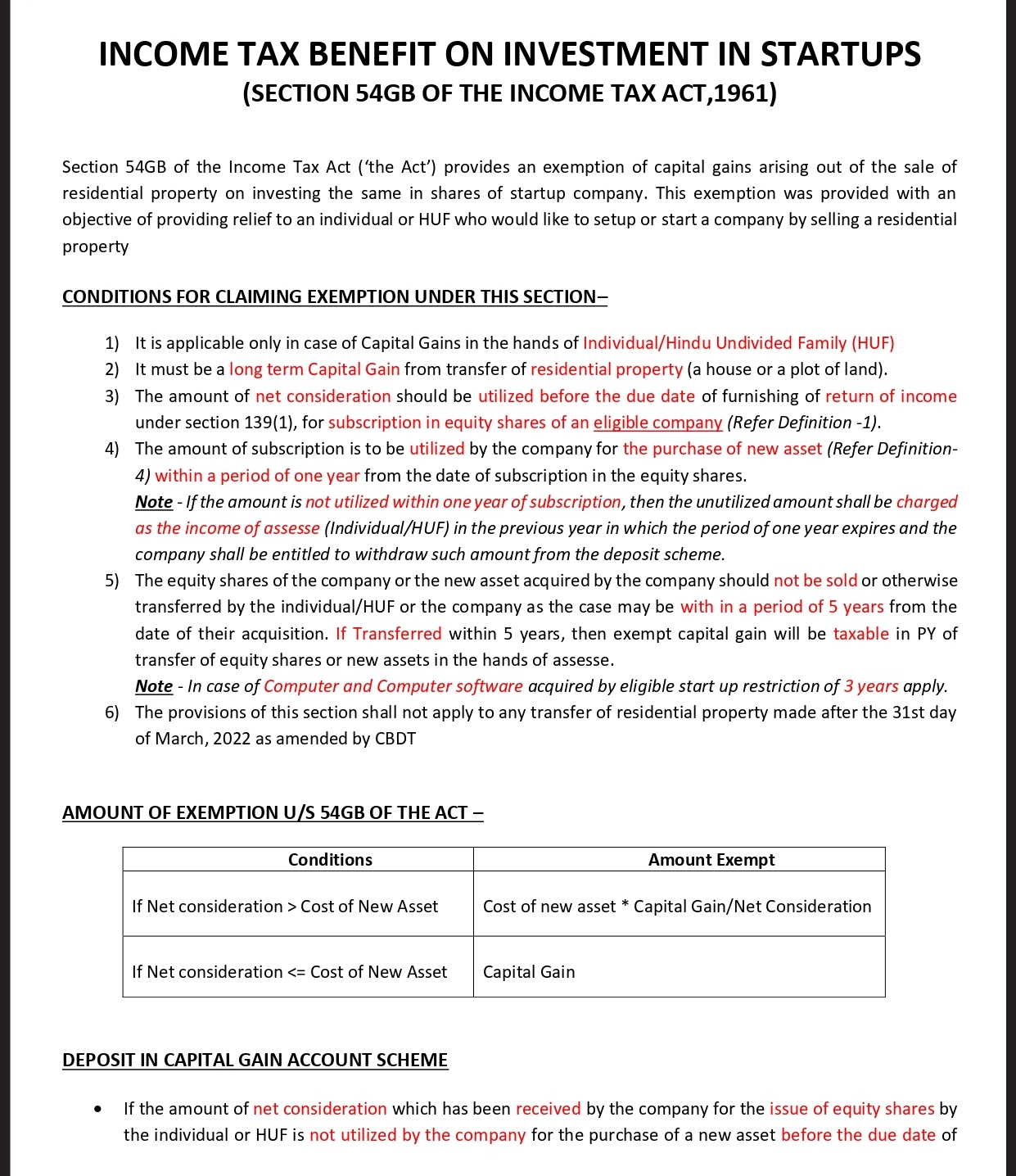

Section 54GB of Income Tax Act Exemption on capital gains from sale of residential property if the proceeds are invested in equity shares of a startup firm. This exemption was created to provide assistance to an individual or HUF who wants to set up or start a business by selling residential property.

- The said income-tax provision under this section 54GB shall not apply to any transfer of residential property made after March 31, 22 modified by Central Board of Direct Taxes

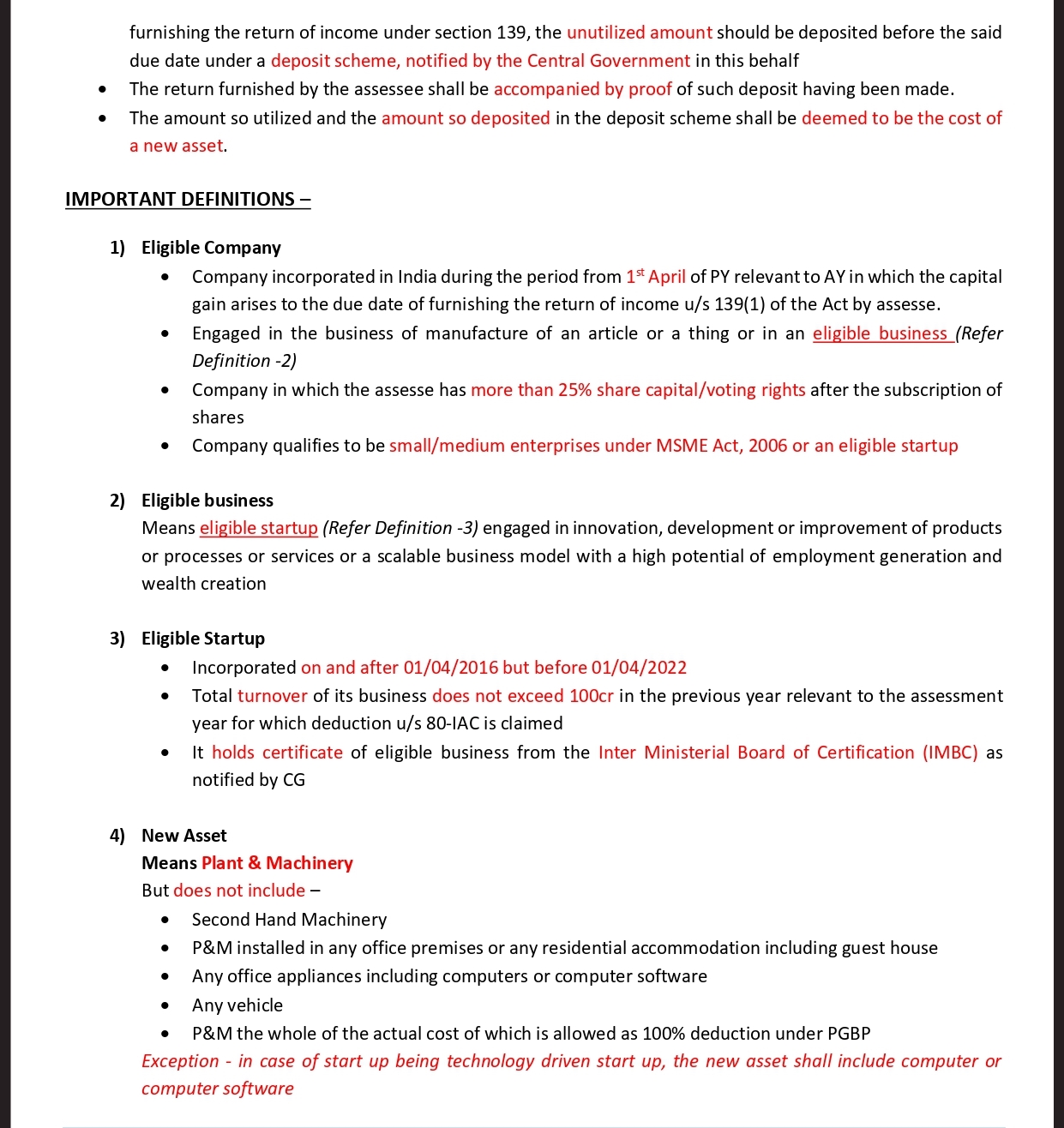

Note – If the amount is not utilized within one year of subscription, it will be taken as income of the assessee (Individual / HUF) in the preceding year in which one year expires, and the amount will be credited to the firm. withdrawal will be allowed. Deposit Scheme.

- Within five years from the date of acquisition, the individual/HUF or the company, as the case may be, should not sell or otherwise transfer the equity shares of the company or any new asset acquired by the firm. If the exempted capital gain is transferred within 5 years, it will be taxable in the hands of the assessee in the PY of transfer of equity shares or new assets.

Note: 3 restrictions apply to the computer and computer software acquired by the qualifying start-up.

- The terms of this clause shall not apply to any residential property transfer made after March 31, 2022, as amended by the CBDT.

Section 54GB. Conditions applicable for claiming exemption under

- It is applicable only on capital gains in the hands of individuals or Hindu Undivided Families (HUFs).

- It must be a long-term capital gain on the sale of a primary residence (a house or a plot of land).

- Net consideration for membership in equity shares of an eligible firm should be utilized before the due date for filing return of income under section 139(1).

- Within one year from the date of subscription in equity shares, the subscription amount should be used by the eligible company for purchase of a new asset.

Exemption amount under section 54GB of Income Tax Act

| Conditions for claiming exemption | discount amount |

| If net consideration > cost of new asset | Cost of New Asset * Capital Gains / Net Considerations |

| If net consideration <= cost of new asset | capital gain |

What are the tax benefits on investment in STARTUPS U/S 54GB?

[ad_2]

Source link