[ad_1]

Full understanding under 80EEA – Housing for all

Budget 2019:

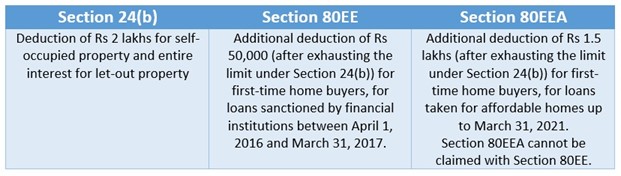

- Introduced in the 2019 Budget, Section 80EEA allows first-time home buyers to save an additional Rs 1.50 lakh per year on home loan interest expenses if they buy an ‘affordable property’. Deduction under section 80EEA exceeds Rs 2,00,000/-, which is the maximum permissible under section 24. (b). But the deduction under section 80EEA is linked to the cost of the house and is available on purchases up to Rs 45 lakh.

- The carpet area of a residence determines its affordability. If a unit is located in a metropolitan city, the carpet area should not exceed 645 square feet (60 sq m) so that the owner can avail the benefits of section 80EEA. The carpet area for flats in any other city has been capped at 968 square feet or 90 square metres.

Budget 2021 Updates:

- The government has officially extended the interest deduction sanctioned for low-cost housing loans availed between April 1, 2019 and March 31, 2022, to achieve the goal of “Housing for All”. Update on Budget 2021: Tax breaks for low-income housing projects have been extended till March 31, 2022.

- Income Tax: With effect from April 1, 2022, the government will no longer provide income tax benefits to first-time home buyers under Section 80EEA. In Budget 2019, the government provided an additional 1.50 lakh income tax credit for home loan borrowers who pay stamp duty of up to 45 lakh for their first property. This facility was extended for one more year in the budgets of 2020 and 2021 respectively.

Section 80EEA and Section 24

- If the owner or his family is residing in the house property, then the owner of the house can claim deduction for interest payment on his home loan up to Rs. 2,00,000/- under section 24 of the Income Tax Act. Deduction up to INR 2,00,000/- is available even if the house is uninhabited. If the property is let out, the full interest on the home loan can be deducted.

- If you meet the requirements of both the sections, you can claim benefits under both Section 24 and Section 80EEA of the Income Tax Act.

- First, use up your deductible limit of Rs 2 lakh under Section 24. Then, we can claim additional benefits under section 80EEA. Consequently, this deduction will be subject to a limit of Rs 2 lakh in addition to section 24.

What is Section 80EEA Exemption?

Deduction under Income Tax Act 1961 for interest paid on housing loan

What is the eligibility under section 80EEA deduction

Budget, 2019, specified eligibility for availing benefits under section 80EEA.

Who can claim u/s 80EEA deduction under Income Tax?

only 1scheduled tribe Time home buyers can avail benefits under this section 80EEA, as it specifically mentions that the borrower should not have any other residential property at the time of issuance of the housing loan.

Who Qualifies as a First Time Home Buyer? 80EEA ,

A first time home buyer is a person who does not have a home in his name when he applies for a mortgage. Even if her parents have a working person’s home, the unmarried is treated as a detached house for tax benefits and thus buys the house for the first time.

What is the deduction available under section 80EEA ,

The exemption under section 80EEA is available only on the interest paid on the home loan.

What is the maximum limit for u/s 80EEA deduction?

The annual deduction limit is INR 1,50,000/-.

What time frame is covered by 80EEA?

The benefits are available to those borrowers whose home loan, when it was sanctioned between April 1, 2019, to March 31, 2022.

What are the conditions for claiming benefits under section 80EEA?

There are certain pre-requisites to apply for claiming tax exemption covered under 80EEA Income Tax Act. They are as follows-

- A loan from a home finance business or FI is required to buy a residential housing property.

- A person cannot be a claimant of section 80EE deduction.

- The stamp duty on residential property should be less than 45 lakhs.

- This should be the buyer’s first purchase. If a house is registered in their name, they will be ineligible for section 80EEA deduction.

- The house loan should be claimed between April 1, 2019, to March 31, 2021.

- The carpet area of a residential property in a metropolitan city should be 645 square feet or more than 60 metres.

- In other cities, the carpet area of a residential site cannot exceed 968 square feet (90 m).

[ad_2]

Source link