People and HUF taxpayers are qualified to choose a new tax regime from F.Y 2020-21.

From F.Y 2020-21, you can choose to pay income tax under a discretionary new tax regime. The new tax regime is accessible for people and HUFs with lower tax rates and zero deductions/exceptions. We will talk about the features of the new tax regime and how you can benefit from it.

1. What’s the amount the new income tax regime for F.Y 2020-21?

The Financial plan F.Y. 2020 presents a new regime under section 115BAC giving a choice to people and HUF taxpayers to pay income tax at lower rates. The new system is appropriate for income earned from 1 April 2020 (F.Y 2020-21), which identifies with A.Y 2021-22.

1. Actual the income tax new rates under the new regime U/s 115 BAC

The tax rates under the new tax regime and the current tax regime are:

Download Automated Income Tax Preparation Excel Based Software All in One for the West Bengal Govt. Employees for the Financial Year 2020-21 and Assessment Year 2021-22 U/s 115BAC

2. Exceptions and deductions not claimable under the new tax regime

The following are the deductions and exceptions you can’t guarantee under the new tax system:

1. The standard deduction, professional tax and amusement allowance on pay rates

2. Leave Travel Allowance (LTA)

3. House Lease Allowance (HRA)

4. Minor kid income allowance

5. Helper allowance

6. Children instruction allowance

7. Other exceptional allowances [Section 10(14)]

8. Interest on lodging advance on the self-involved property or empty property (Section 24)

9. Chapter VI-A deduction (80C,80D, 80E, etc) (Aside from Section 80CCD(2) and 80JJAA)

10. Without exception or deduction for any different perquisites or allowances

11. Deduction from family annuity income

What are the exceptions and deductions accessible under the new regime?

You can tax exclusion for:

1. Transport allowances if there should arise an occurrence of a specially-abled individual.

2. Conveyance allowance got to meet the conveyance use brought about as a major aspect of the employment.

3. Any pay got to meet the expense of movement on visit or transfer.

3. Would I be able to choose between the new tax regime and

the current regime?

An employee can choose the new tax regime toward the start of F.Y 2020-21 and personal their employer. The employee can’t change their decision anytime during the financial year. Be that as it may, the change should be possible at the hour of filing the income tax return on 31st December 2020. ( Extended the Return Filling by the CBDT)

On the off chance that an employee doesn’t choose the new tax regime toward the start of the financial year, the employer will deduct tax (TDS) under the current tax regime.

A salaried taxpayer can pick in and quit every year. That implies you can choose the new tax regime in one year and choose the standard tax regime in one more year.

A non-salaried taxpayer needs to choose the new regime at the hour of filing the tax return. They need not pronounce or close their decision to anyone whenever during the year. In any case, a non-salaried taxpayer can’t select in and quit the new tax regime every year. When a non-salaried quits the new tax regime, they can’t pick in again for the new tax regime in the future.

4. House property misfortune under the new tax regime

If there should be an occurrence of a self-involved property, you can’t guarantee a deduction on enthusiasm for a lodging credit under the new tax regime. The deduction of Rs 2 lakh permitted in the current system isn’t accessible in the new tax regime. You can’t set-off the loss of Rs 2 lakh from house property from your salary income.

If you have let-out a house property, you can guarantee a deduction for intrigue paid on the lodging advance. Do take note of that the new tax regime limits the deduction to the taxable lease got from the property. You can’t set-off the misfortune emerging from the house property because of the overabundance of intrigue paid over the rental income. Likewise, you can’t carry forward the misfortune from house property to future years for set off.

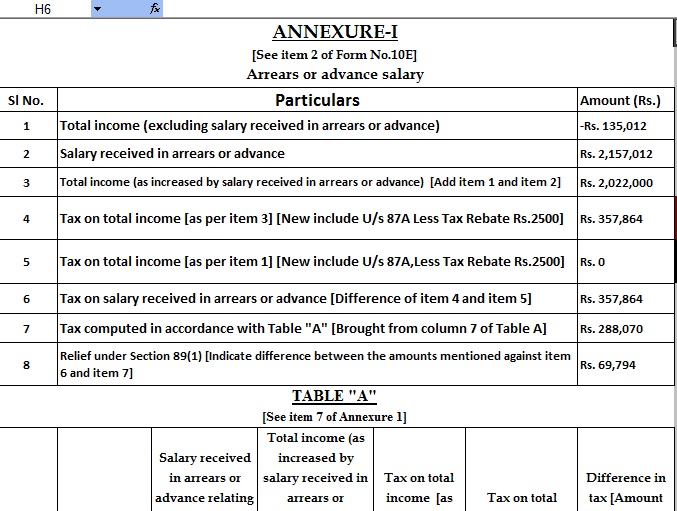

Download Automated Income Tax Arrears Relief Calculator U/s 89(1) along with Form 10E from the Financial Year 2000-01 to Financial Year 2020-21 (Up-to-date Version)