[ad_1]

NBFC Types, Fundamental Analysis, Key Ratios and Fundamental Concerns

Classification of NBFCs on the basis of activities.

investment activities

- lending activities

- credit related activities

- investment company

- Non-Operative Financial Holding Company

- Core Investment Company

Lending related activities and activities:

- 1. Asset Finance Company

- infrastructure debt company

- micro finance company

- with loan

- infrastructure finance company

- factors

other activities

- P2P (Peer to Peer) Lending Platform

- mortgage guarantee company

- account aggregator

What are the documents required to get NBFC license in India?

Mandatory Documents Required for Obtaining NBFC License in India

Following is the list of documents which are required to be submitted with RBI for purchase:

- Adequate copy of commencement of business certificate and certificate of incorporation of the company.

- Director’s Statement to be filled and signed by each of the Directors of the Company.

- Certificate of Directors from NBFCs, where the directors have worked in the past, showing experience.

- Adequate replica of the Memorandum of Association (MOA) of the Association of Associations (AOA) of the company

- CIBIL data of directors of the company.

- Verify the Board’s resolution under the Fair Practices Code.

- Board resolution specifically to submit the application and authorize the signatory.

- Adequate copy of Company’s Permanent Account Number and Company Identification Number.

- Resolution of the Board to prove that the company has no deposits and has not accepted any public deposits.

- Further, it will also be stated that it will not accept any deposits in the near future without obtaining approval from the Reserve Bank of India.

- Board resolution to prove that the company does not have any unregistered NBFCs

- Evidence that no business activities are being carried out without registering with RBI.

- Financial statements relating to the last 2 years of unincorporated bodies.

- A list including the authorized share capital and the new shareholding of the enterprise

- Net owned funds should also be mentioned along with the fixed deposit receipt and bank details.

- Statement of Profit and Loss Account and Audited Balance Sheet for the three years along with the reports of Directors and Auditors.

- All details of bank accounts and postal address of the bank, loan/credit facilities.

- Bank statement and income tax return self attested by the company.

- The business plan of the firm for the next three years which should include essential details about the business, balance sheet, market segment etc.

NBFC Registration Process for Obtaining NBFC License in India

The registration process consists of certain steps that must be followed to obtain an NBFC license. Licensing is important for the smooth establishment of the company. NBFC license plays an essential role and it should be acquired after following the NBFC registration process mentioned below –

- Registering a company before filing an application: The first step in obtaining an NBFC license is the registration of the company. The company must be registered as per the Companies Act 2013 or the Companies Act 1956.

- Ownership of Net Owned Funds: The company should have minimum Net Owned Funds (NOF). The amount should be Rs 2 crore or more.

- Presence of Directors: The company should have at least one director.

- CIBIL Score: Maintaining a good CIBIL score is essential as it is an important aspect that is considered and it fulfills the eligibility requirements to register as an NBFC.

- File Application Form: The next step in the process is to file an application form on the RBI website.

- Submission of Important Documents: Next, the applicant has to submit all the required documents along with the application form.

- Obtaining CARN Number: After submitting the application form and documents, a CARN number will be provided to the applicant.

- Submission of Application Form: The hard copy of the application has to be submitted to the regional branch of RBI.

- Arrival of NBFC License: Once the application is approved and verified, the license will be granted to the company

NBFC Fundamental Analysis and Key Ratios

- Non-Banking Financial Companies (NBFCs) are businesses that provide banking services at low cost. They are in the lending and advances industry, as well as in the acquisition of shares, shares, bonds, debentures, government securities, and other marketable securities of lease and insurance. Firms are required to obtain an NBFC license to form an NBFC.

- Fundamental analysis is basically an evaluation to understand the financial position of a company. The various aspects that are evaluated include cash flow, projected earnings, debt/equity ratio, return on income, return on investment, etc.

Steps to Perform Fundamental Analysis of a Company

- understand the nature of the business

- Understand the scope of the company’s development

- Identify the company’s products or services and identify whether it has the potential to expand and grow.

- Analyze and evaluate the factors that explain the financial position of the company. Annual reports are a great way to identify where a company stands financially. Evaluate important details like profit and loss statement, balance sheet, cash flow statement etc.

- Complete the appraisal process and understand the debt ratio

- Identify the company’s competitors

Framework on Methods of Fundamental Analysis of NBFCs

net interest margin: To explain more clearly the net interest margin is the difference between the interest paid and the interest received.

nim = . formula to calculate Net Interest Margin Investment Return – Interest expense / average earning asset.

net profit margin: It shows How much profit is earned as a percentage of total revenue.

npm = . formula to calculate net profit/sales

return on assets= Shows how much profit is generated from the asset. It is one of the profitability ratios which is helpful in checking the functioning of NBFCs.

Return on Asset Formula = Net Profit / Average Net Worth

return on equity = It is equal to the return earned by the shareholders of the company

Financial Ratio

- current ratio: CR = Current Assets / Current Liabilities

- Dividend:ROE = Net Income / Shareholder’s Equity

- Debt to Equity Ratio: DE =Total Liabilities / Shareholders Equity

- Dividend:ROE = Net Income / Shareholder’s Equity

- quick ratio: QR = (Current Assets – Inventory) / Current Liabilities

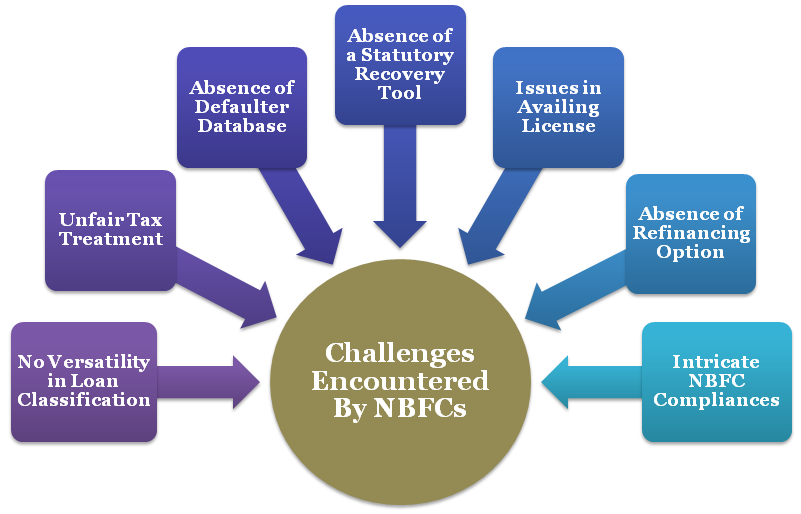

Fundamental Issues/Problems for the Non-Banking Financial Institution Sector

The NBFC sector faces various issues and challenges in its functioning. Some of the major concerns of the NBFC sector are; An NBFC has to register itself with all the four CICs like any other credit institution like a bank and if it does not become a member, it becomes a cause for concern. Also, we will see how they can avoid any kind of disruption in their work by following the prescribed guidelines. Also, in this blog, we are going to look at some common concerns. NBFC Sector And what are the guidelines laid down by the relevant regulatory bodies.

General Issues/Concerns of the NBFC Sector: Following are some of the concerns of the NBFC sector in India.

- There are 4 CICs and the matter of concern is that the NBFC is not registered with all 4 of them.

- It has been made mandatory for all credit institutions including NBFCs to become a member of 4 CICs through limited credit information bureaus by RBI.

The rules are:

- RBI gave a period of 3 months to all credit institutions to become members of the CIC. CICs update the credit information on a monthly basis to keep a record of it.

- No registration of CKYCR

- CKYCR is a repository of KYC details of the customers. It aims to reduce the process and burden of preparation of KYC documents and periodic verification of each new customer who signs with the financial sector.

The criteria are:

- Compulsory for NBFCs to register with CKYCR. Regulated entities like NBFCs are subject to mandatory regulation to comply with KYC norms. Non-banking financial institutions and all payment system providers are some of the other regulated entities.

3. No prior approval from RBI by NBFC for change of name.

- The Reserve Bank of India has observed that many NBFCs were adamant on changing their names without informing the banks. InfoTech at the end of the name of the NBFC was used by many to gain unfair advantage.

The criteria are:

- RBI advised and made it mandatory to inform regulatory bodies in case of NBFC name change for any reason. Change of names makes it necessary for any NBFC to take prior approval from RBI so as to avoid the misuse associated with it.

- Non-Banking Financial Companies which are not complying with the same are liable to penalty in the form of cancellation if the certificate of registration is already registered or rejection of application for registration, if not registered.

- Sources of NBFCs need to be shown.

- Unlike banks, the sources of financing of NBFCs are not dependent on current account savings as a source of income. Alternative sources of funding should be explored.

The criteria are:

- There are some business activities permitted by NBFCs by RBI, such as loan advance insurance of share bonds etc.

- It is mandatory for NBFCs to report to RBI as to the source of their funding.

- Not following KYC guidelines

- Know Your Customer (KYC) is basically an international benchmark used for framing anti money laundering regulations and it is also used by regulatory bodies to combat terrorism financing.

The criteria are:

- All NBFCs are said to carry out certain exercises as per the guidelines and ensure formation of KYC and Anti-Money Laundering measures within the organization by appropriate approval from their Board.

- Non-compliance with credit exposure limit

- Credit exposure limit basically occurs when a lender makes some amount available by the lender to the borrower which is called credit exposure limit. It shows the extent to which the lender may be at risk of loss in case of a defaulting borrower.

The criteria are:

- RBI guidelines suggest that the single borrower limit should be fixed at 15%. It used to be 10% for NBFCs not for infrastructure financing.

- Do not stick to leverage limits

- The leverage limit is the total putside liabilities of the net-owned funds by RBI. This was stipulated by the said institution on 7 that no NBFC should exceed this limit. From 31st March 2015.

- Inability to produce records on demand due to poor record keeping.

- Poor record keeping can be a loss agenda for any company. It causes loss of time, inefficiency and unnecessary stress.

The criteria are:

- The new Indian Accounting Norms as of 2018 mandate that all NBFCs including housing finance companies have to set aside some amount in the form of provisions, the impact of which is felt on the bottom line. Anticipated credit loss is one method on which credit loss provisioning criteria should be built.

- Aggressive marketing strategy with utilization of low quality manpower.

RBI made some rules regarding the advertisement of NBFCs. It is used to promote the business of NBFCs or to seek various services.

The criteria are:

RBI has stipulated that all advertisements for NBFCs should contain the following:

- Mode of repayment of deposit

- All terms and conditions relating to deposit renewal

- Deposit not mentioned insured

- Any other feature relating to the terms and conditions of acceptance of deposits.

some other concerns

- No prior approval of RBI is required within 30 days in case of change in management

- NBFC does not notify the statutory auditor about the change

- NBFC not taking prior approval of change in control and management

- If there is a change in management there is no information where prior approval of RBI is not required

- NBFC not providing copy of loan agreement to borrower, interest rates not mentioned in annualized form, no display of grievance redressal metrics in branches and official website

- The correspondence email id of the company should be the same as that registered with MCA

- NBFC sector is not present at the registered address

- Submission of incomplete documents while applying for prior approval

- NBFCs delayed reply to correspondence sent by RBI

[ad_2]

Source link