[ad_1]

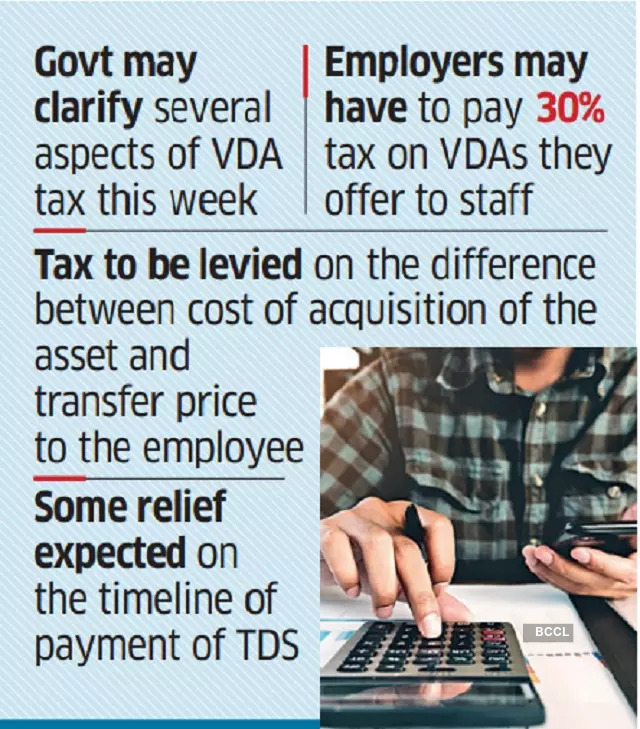

A government official said, “The rules are being worked out…these will be issued soon.” ET had earlier reported that credit card reward points and e-voucher VDA will not be considered. The clarification is expected to clearly outline the principles for determining the cost of acquisition of VDAs.

Government is examining whether the first-in-first-out method adopted for demat securities, weighted average or last-in-first-out format should be considered for determining cost of acquisition .

The clarification may also provide some relief on the payment timelines tax deducted at source (TDS). Another official said, “The clarification will address some of the concerns raised by the industry.”

In the FY23 budget presented in February, the government brought VDA under the tax net. Any income arising from transfer of any VDA with effect from 1st April attracts 30% flat tax. In addition, 1% Tax at Source (TDS) is to be deducted on transactions in such asset classes above a certain limit. 1% TDS to be applicable from 1st July.

The crypto industry has asked the government for relaxation of TDS conditions which require payment before issue of consideration in cryptocurrency or other VDA Transactions, The industry wants tax to be allowed to be paid on or before the due date for payment of TDS.

Sudhir Kapadia, National Tax Leader, EY, said, “With respect to TDS at 1% on transfer of VDA or in return, it is not technically possible to ensure payment of tax before issue of consideration as such exchange happens immediately.” “It should be clarified that tax can be paid as per the normal due dates for TDS payment.”

Under the existing provisions, TDS has to be deposited by the 7th day of the following month. For example, if a transaction on which TDS is applicable happens on October 21, then the amount deducted has to be deposited by November 7. TDS can be deposited only in the case of March, in the last month of the financial year, up to April. 30.

[ad_2]

Source link